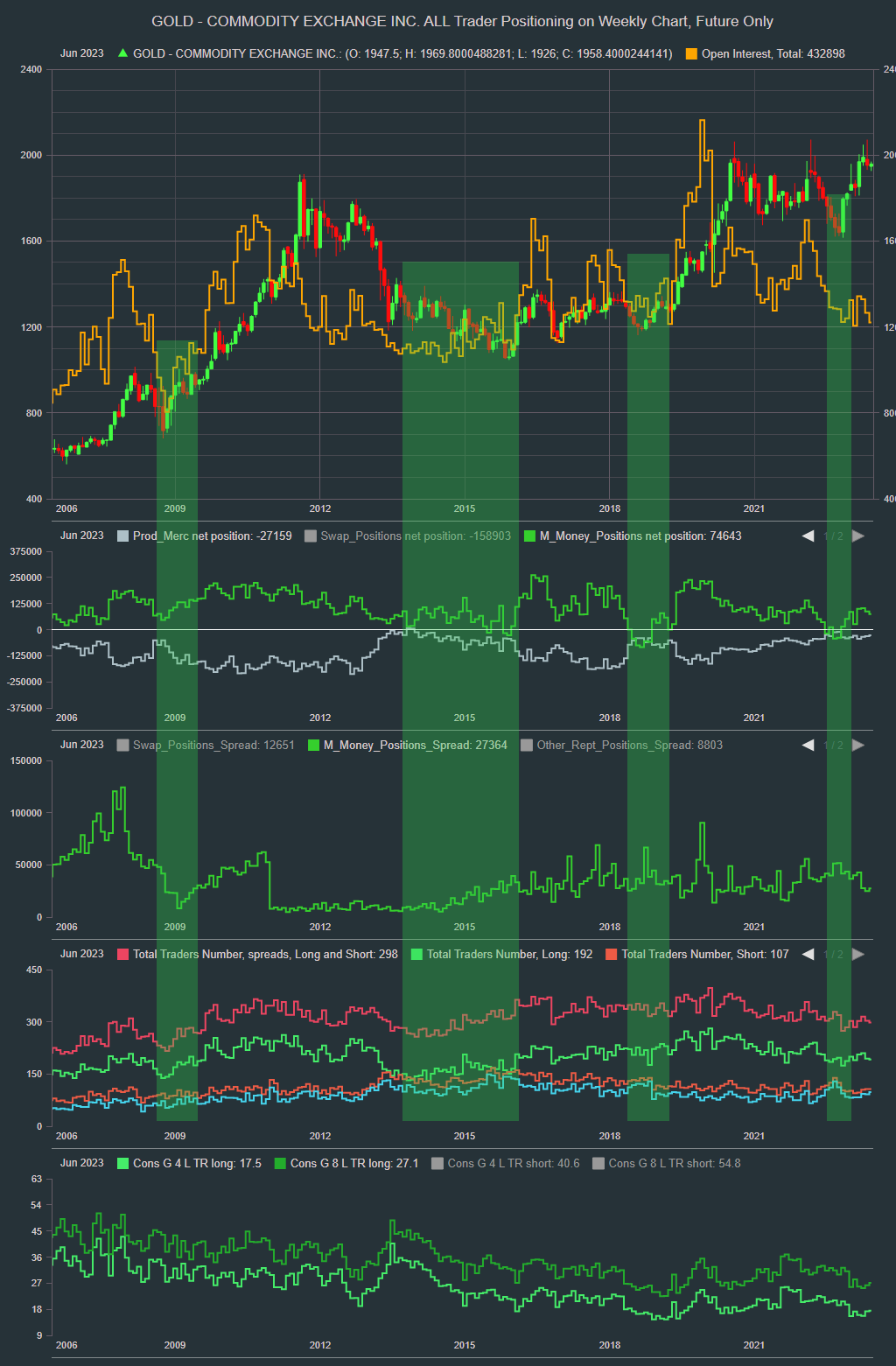

Open interest

Open interest is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc. The aggregate of all long open interest is equal to the aggregate of all short open interest.

Open interest held or controlled by a trader is referred to as that trader’s position. For the COT Futures-and-Options-Combined report, option open interest and traders’ option positions are computed on a futures-equivalent basis using delta factors supplied by the exchanges. Long-call and short-put open interest are converted to long futures-equivalent open interest. Likewise, short-call and long-put open interest are converted to short futures-equivalent open interest. For example, a trader holding a long put position of 500 contracts with a delta factor of 0.50 is considered to be holding a short futures-equivalent position of 250 contracts. A trader’s long and short futures-equivalent positions are added to the trader’s long and short futures positions to give “combined-long” and “combined-short” positions. Open interest, as reported to the Commission and as used in the COT report, does not include open futures contracts against which notices of deliveries have been stopped by a trader or issued by the clearing organization of an exchange.

Reportable positions

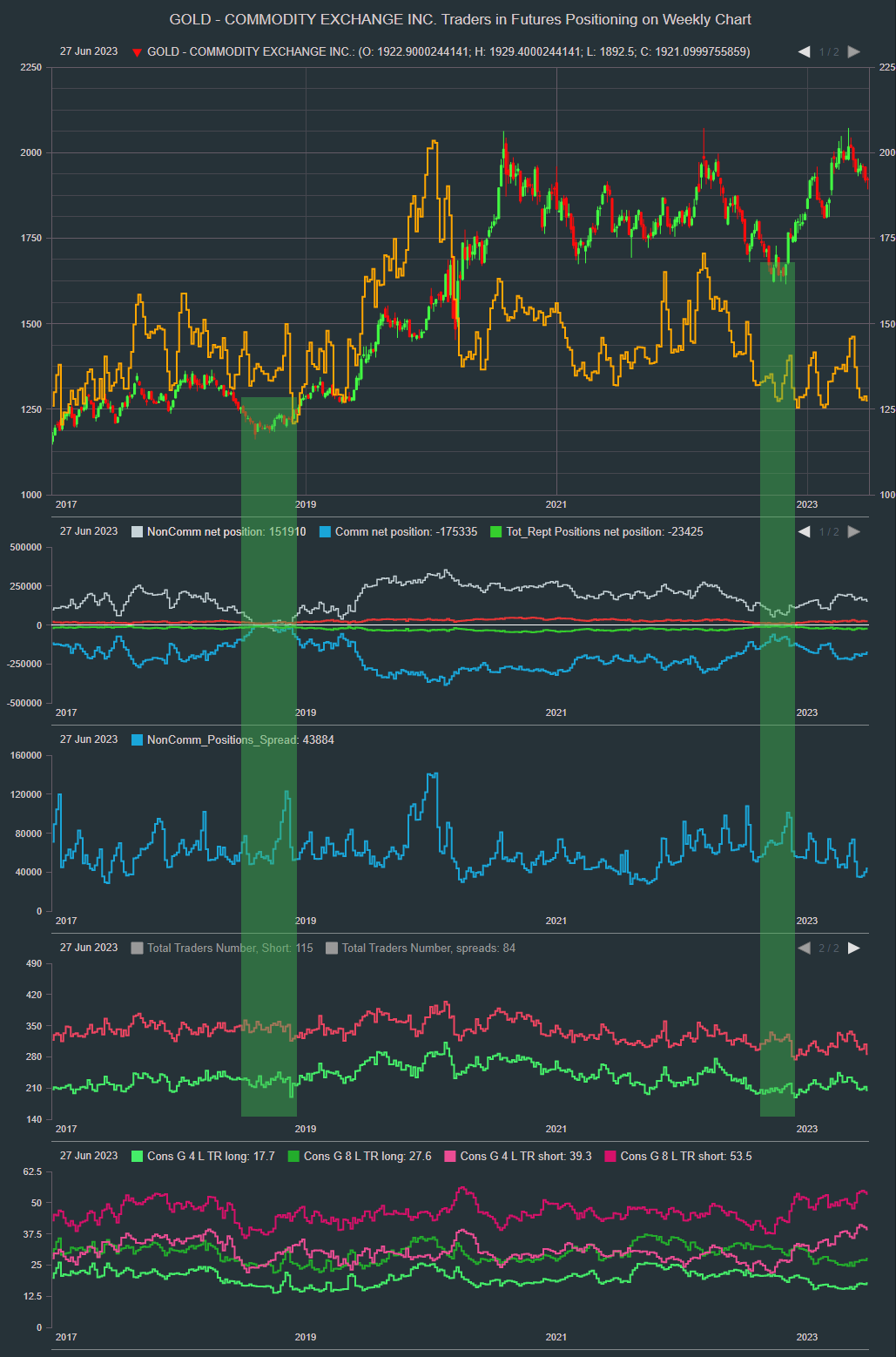

Clearing members, futures commission merchants, and foreign brokers (collectively called reporting firms) file daily reports with the Commission. Those reports show the futures and option positions of traders that hold positions above specific reporting levels set by regulations. If, at the daily market close, a reporting firm has a trader with a position at or above the Commission’s reporting level in any single futures month or option expiration, it reports that trader’s entire position in all futures and options expiration months in that commodity, regardless of size. The aggregate of all traders’ positions reported to the Commission usually represents 70 to 90 percent of the total open interest in any given market. From time to time, the Commission will raise or lower the reporting levels in specific markets to strike a balance between collecting sufficient information to oversee the markets and minimizing the reporting burden on the futures industry.

Commercial and Non-commercial Traders

When an individual reportable trader is identified to the Commission, the trader is classified either as “commercial” or “non-commercial.” All of a trader’s reported futures positions in a commodity are classified as commercial if the trader uses futures contracts in that particular commodity for hedging. A trading entity generally gets classified as a “commercial” trader by filing a statement with the Commission that it is commercially “…engaged in business activities hedged by the use of the futures or option markets.” To ensure that traders are classified with accuracy and consistency, Commission staff may exercise judgment in re-classifying a trader if it has additional information about the trader’s use of the markets. A trader may be classified as a commercial trader in some commodities and as a non-commercial trader in other commodities. A single trading entity cannot be classified as both a commercial and non-commercial trader in the same commodity. Nonetheless, a multi-functional organization that has more than one trading entity may have each trading entity classified separately in a commodity. For example, a financial organization trading in financial futures may have a banking entity whose positions are classified as commercial and have a separate money-management entity whose positions are classified as non-commercial.

Nonreportable Positions

The long and short open interest shown as “Nonreportable Positions” is derived by subtracting total long and short “Reportable Positions” from the total open interest. Accordingly, for “Nonreportable Positions,” the number of traders involved and the commercial/non-commercial classification of each trader are unknown.

Spreading

For the futures-only report, spreading measures the extent to which each non-commercial trader holds equal long and short futures positions. For the options-and-futures-combined report, spreading measures the extent to which each non-commercial trader holds equal combined-long and combined-short positions. For example, if a non-commercial trader in Eurodollar futures holds 2,000 long contracts and 1,500 short contracts, 500 contracts will appear in the “Long” category and 1,500 contracts will appear in the “Spreading” category. These figures do not include intermarket spreading, such as spreading Eurodollar futures against Treasury Note futures.

Number of Traders

To determine the total number of reportable traders in a market, a trader is counted only once whether or not the trader appears in more than one category (non-commercial traders may be long or short only and may be spreading; commercial traders may be long and short). To determine the number of traders in each category, however, a trader is counted in each category in which the trader holds a position. The sum of the numbers of traders in each category, therefore, will often exceed the number of traders in that market.

Concentration Ratios

The report shows the percents of open interest held by the largest four and eight reportable traders, without regard to whether they are classified as commercial or non-commercial. The concentration ratios are shown with trader positions computed on a gross long and gross short basis and on a net long or net short basis. The “Net Position” ratios are computed after offsetting each trader’s equal long and short positions. A reportable trader with relatively large, balanced long and short positions in a single market, therefore, may be among the four and eight largest traders in both the gross long and gross short categories, but will probably not be included among the four and eight largest traders on a net basis.

Supplemental Report

the Supplemental report shows an additional category of “Index Traders” in selected agricultural markets. These traders are drawn from the noncommercial and commercial categories. The noncommercial category includes positions of managed funds, pension funds, and other investors that are generally seeking exposure to a broad index of commodity prices as an asset class in an unleveraged and passively-managed manner. The commercial category includes positions for entities whose trading predominantly reflects hedging of over-the-counter transactions involving commodity indices—for example, a swap dealer holding long futures positions to hedge a short commodity index exposure opposite institutional traders, such as pension funds.

All of these traders—whether coming from the noncommercial or commercial categories—are generally replicating a commodity index by establishing long futures positions in the component markets and then rolling those positions forward from future to future using a fixed methodology. Some traders assigned to the Index Traders category are engaged in other futures activity that could not be disaggregated. As a result, the Index Traders category, which is typically made up of traders with long-only futures positions replicating an index, will include some long and short positions where traders have multi-dimensional trading activities, the preponderance of which is index trading. Likewise, the Index Traders category will not include some traders who are engaged in index trading, but for whom it does not represent a substantial part of their overall trading activity.

TRADERS IN FINANCIAL FUTURES

The new report separates large traders in the financial markets into the following four categories: Dealer/Intermediary; Asset Manager/Institutional; Leveraged Funds; and Other Reportables. The legacy COT report separates reportable traders only into “commercial” and “noncommercial” categories.

The TFF report divides the financial futures market participants into the “sell side” and “buy side.” This traditional functional division of financial market participants focuses on their respective roles in the broader marketplace, not whether they are buyers or sellers of futures/option contracts. The category called “dealer/intermediary,” for instance, represents sellside participants. Typically, these are dealers and intermediaries that earn commissions on selling financial products, capturing bid/offer spreads and otherwise accommodating clients. The remaining three categories (“asset manager/institutional;” “leveraged funds;” and “other reportables”) represent the buy-side participants. These are essentially clients of the sell-side participants who use the markets to invest, hedge, manage risk, speculate or change the term structure or duration of their assets.

Dealer/Intermediary

These participants are what are typically described as the “sell side” of the market. Though they may not predominately sell futures, they do design and sell various financial assets to clients. They tend to have matched books or offset their risk across markets and clients. Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities. These include large banks (U.S. and non-U.S.) and dealers in securities, swaps and other derivatives.

The rest of the market comprises the “buy-side,” which is divided into three separate categories:

Asset Manager/Institutional

These are institutional investors, including pension funds, endowments, insurance companies, mutual funds and those portfolio/investment managers whose clients are predominantly institutional.

Leveraged Funds

These are typically hedge funds and various types of money managers, including registered commodity trading advisors (CTAs); registered commodity pool operators (CPOs) or unregistered funds. The strategies may involve taking outright positions or arbitrage within and across markets. The traders may be engaged in managing and conducting proprietary futures trading and trading on behalf of speculative clients.

Other Reportables

Reportable traders that are not placed into one of the first three categories are placed into the “other reportables” category. The traders in this category mostly are using markets to hedge business risk, whether that risk is related to foreign exchange, equities or interest rates. This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

Spreading

The TFF sets out open interest by long, short, and spreading for all four categories of traders. “Spreading” is a computed amount equal to offsetting long and short positions held by a trader. The computed amount of spreading is calculated as the amount of offsetting futures in different calendar months or offsetting futures and options in the same or different calendar months. Any residual long or short position is reported in the long or short column. Inter-market spreads are not considered.

Numbers of Traders

The sum of the numbers of traders in each separate category typically exceeds the total number of reportable traders. This results from the fact that “spreading” can be a partial activity, so the same trader can fall into either the outright “long” or “short” trader count as well as into the

“spreading” count. In order to preserve the confidentiality of traders, for any given commodity where a specific category has fewer than four active traders, the size of the relevant positions will be provided but the trader count will not be (specifically, a “·” will appear for trader counts of fewer than four traders).

Disaggregated Commitments of Traders Report

The Disaggregated COT report increases transparency from the legacy COT reports by separating traders into the following four categories of traders: Producer/Merchant/Processor/User; Swap Dealers; Managed Money; and Other Reportables. The legacy COT report separates reportable traders only into “commercial” and “non-commercial” categories.

The Commission, by regulation, collects confidential daily large-trader data as part of its market surveillance program. The data, which also support the legacy COT report, is separated into the following categories:

1) “Producer/Merchant/Processor/User,”

2) “Swap Dealers,”

3) “Managed Money,” and

4) “Other Reportables.”

Producer/Merchant/Processor/User

A “producer/merchant/processor/user” is an entity that predominantly engages in the production, processing, packing or handling of a physical commodity and uses the futures markets to manage or hedge risks associated with those activities.

Swap Dealer

A “swap dealer” is an entity that deals primarily in swaps for a commodity and uses the futures markets to manage or hedge the risk associated with those swaps transactions. The swap dealer’s counterparties may be speculative traders, like hedge funds, or traditional commercial clients that are managing risk arising from their dealings in the physical commodity.

Money Manager

A “money manager,” for the purpose of this report, is a registered commodity trading advisor (CTA); a registered commodity pool operator (CPO); or an unregistered fund. These traders are engaged in managing and conducting organized futures trading on behalf of clients.

Other Reportables

Every other reportable trader that is not placed into one of the other three categories is placed into the “other reportables” category.

Spreading

The Disaggregated COT sets out open interest by long, short, and spreading for the three categories of traders—“swap dealers,” “managed money,” and “other reportable.” For the “producer/merchant/processor/user” category, open interest is reported only by long or short positions. “Spreading” is a computed amount equal to offsetting long and short positions held by a trader. The computed amount of spreading is calculated as the amount of offsetting futures in different calendar months or offsetting futures and options in the same or different calendar months. Any residual long or short position is reported in the long or short column. Inter-market spreads are not considered.

Numbers of Traders

The sum of the numbers of traders in each separate category typically exceeds the total number of reportable traders. This results from the fact that, in the “swap dealers,” “managed money,” and “other reportables” categories, “spreading” can be a partial activity, so the same trader can fall into either the outright “long” or “short” trader count, as well as into the “spreading” count. Additionally, a reportable “producer/merchant/processor/user” may be in both the long and the short position columns. In order to preserve the confidentiality of traders, for any given commodity where a specific category has fewer than four active traders, the size of the relevant positions will be provided but the trader count will be suppressed (specifically, a “·” will appear for trader counts of fewer than four traders).

An unregistered fund may have a Part 4 exclusion from CTA/CPO registration or be a non-U.S. entity that is unregistered. So called “hedge funds” are included in this category, regardless of whether they are registered.